Published On Dec 22, 2020

#datascience #machinelearning #timeseries

Detailed video on ADF test - • Time Series Non Stationary Statistica...

Detailed video on granger causality - • Granger Causality Statistical Test fo...

You can watch my entire time series here - • Time Series Modelling and Analysis

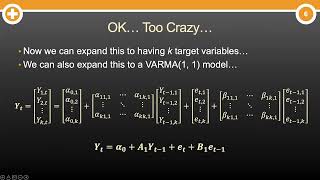

Vector autoregression (VAR) is a statistical model used to capture the relationship between multiple quantities as they change over time

VAR models (vector autoregressive models) are used for multivariate time series. The structure is that each variable is a linear function of past lags of itself and past lags of the other variables

The Granger causality test is a statistical hypothesis test for determining whether one time series is useful in forecasting another

The Augmented Dickey Fuller Test (ADF) is unit root test for stationarity. Unit roots can cause unpredictable results in your time series analysis.