Published On Apr 1, 2019

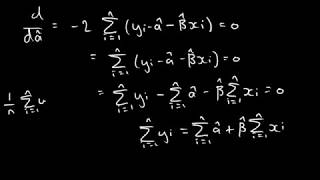

I derive the mean and variance of the sampling distribution of the slope estimator (beta_1 hat) in simple linear regression (in the fixed X case). I discuss the typical model assumptions, and discuss where we use them as I carry out the derivations. The derivations are carried out using summation notation (no matrices).

At the end, I briefly discuss the normality assumption, and how that leads to beta_1 hat being normally distributed. While I do discuss the real deal there, I go over it fairly quickly, as the main point of the video is deriving E(beta_1 hat) and Var(beta_1 hat).

Note that any time I use "errors" or "error terms" in this video, I am referring to the theoretical error terms (the epsilons) and not observed residuals from sample data.

Time stamps:

0:00 Brief discussion the simple linear regression model, assumptions, and some tools we will use.

2:58 Deriving E(beta_1 hat)

5:06 Deriving Var(beta_1 hat)

8:49 Discussion of normality of beta_1 hat.